12.

Published onThe responses to the following information requests were taken into account in determining the assigned category and developing the assessment:

Ministry of Energy

https://drive.google.com/file/d/1R2DVDIEcqLcYp8z66G7UsopAj8QERrDO/view?usp=drive_link

Further information:

Global context: goal and progress

The goal of tripling global installed renewable energy capacity by 2030 was one of the main agreements reached at the 28th Conference of the Parties (COP28) to the UN Framework Convention on Climate Change (UNFCCC), held in Dubai in December 2023. While not legally binding, the goal was endorsed by more than 130 countries and was included in the final Global Stocktake document, the mechanism that assesses collective progress under the Paris Agreement.

The proposal to triple renewables and double energy efficiency by 2030 emerged as a technical recommendation from international organizations as a necessary condition to keep the 1.5°C limit within reach (IEA, 2023; IRENA, 2023). In line with the tripling goal and the Paris Agreement temperature target, global renewable capacity must reach 11.5 terawatts (TW) by 2030, a 3.4-fold increase over 2022 levels.

Despite the acceleration in renewable deployment (growth of 14% in 2023 and 15% in 2024), current progress remains insufficient relative to the required trajectory. If capacity additions continued to grow at 14% annually through 2030, the shortfall from the 11.2 TW objective would be 1.5 TW—roughly equivalent to today’s combined installed renewable capacity of Europe, North America, Oceania, the Middle East, Africa, Central America, and the Caribbean (Global Renewables Alliance, 2024; IRENA, 2024).

IEA (2024) notes that only 14 countries included explicit renewable capacity targets for 2030 in their NDCs, and that the committed additions amount to around 1,300 GW globally—just 12% of the 11,000 GW needed to achieve the tripling set at COP28.

Regional context: implications of subscribing to the pledge and assessment of Argentina’s alignment

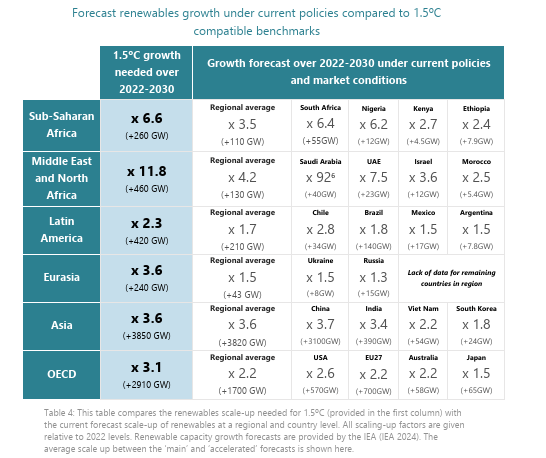

However, this aggregate global challenge does not translate linearly to regional and national levels. To triple global installed renewable capacity by 2030, different regions will need to scale at different rates, depending on their current renewable capacity, the speed at which they must phase out fossil fuels, and projected growth in electricity demand (Climate Analytics, 2024).

According to Climate Analytics (2024) projections, Latin America should multiply renewable generation by 2.3. However, under current policies and market conditions, Argentina is expected to increase its renewable generation capacity by 7.8 GW between 2022 and 2030, which represents only a 1.5-fold increase over 2022 levels.

By comparison, Brazil—whose power mix is considerably cleaner than Argentina’s—projects a 1.8-fold increase in generation from non-conventional renewables.

Table 1. Projected renewable generation 2022–2030 under current policies and market conditions.

Source: Climate Analytics, 2024.

According to the IEA’s COP28 Tripling Renewable Capacity Pledge report, Latin America as a whole projects a 39% increase in renewable capacity by 2030, reaching nearly 450 GW. While Brazil, Mexico, Chile, and Argentina account for roughly 80% of the projected regional total, their levels of ambition differ markedly.

Chile leads in relative terms, with an estimated 2.5-fold increase over its current capacity, followed by Mexico and Brazil. Argentina, by contrast, shows one of the more modest expansion levels within the group, with projected growth below the regional average—placing it among the countries with lower relative ambition under the global pledge to triple renewable capacity by 2030.

For Argentina specifically, the IEA projects that the share of non-conventional renewables in the electricity mix will rise from 12% in 2023 to 23% in 2030, driven mainly by the build-out of large solar and wind farms

These projections are largely explained by the lack of clear signals from national energy policy. At present, no new concrete targets have been set for the expansion of renewable energy, which undermines predictability for the sector. This is compounded by the absence of an integrated plan to resolve the bottleneck in the high-voltage transmission system—an essential condition for enabling new large-scale renewable projects—whose expansion, even in the best-case scenario, will require several years of planning, investment, and implementation.

Wholesale Electricity Market Annual Report

FIRST ASSESSMENT OF THIS OBJECTIVE CONDUCTED IN AUGUST 2025

Category

Early progress

Detail

Although the objective of reaching at least 11,000 GW of installed renewable energy generation capacity worldwide by 2030 is a global commitment, its achievement requires coordinated efforts by each country, according to their capacities, challenges and national circumstances. Argentina has the potential to make a significant contribution: the country has some of the world’s best wind resources in Patagonia, as well as excellent solar conditions in north-western Argentina and the Cuyo region. However, this contribution is currently constrained by structural barriers.

In 2024, Argentina had 6,672 MW of installed non-conventional renewable energy capacity, accounting for 15% of the electricity mix (CAMMESA, 2025). Law No. 27,191 of 2015 established a target of 20% non-conventional renewable energy by 2025. No new specific targets have subsequently been established for the expansion of renewable energy, weakening predictability for the sector.

In addition, there is no comprehensive plan to address the bottleneck in the high-voltage electricity transmission system, which is an essential condition for enabling new large-scale renewable energy projects. Even under the most favourable scenario, expanding this infrastructure would require several years of planning, investment and implementation. Therefore, the objective is classified as “Early progress”.